Definition and Scope of Economics

Economics has been defined in numerous ways by different economists throughout history. Each economist views the subject through their unique perspective, resulting in definitions that reflect their particular interests and focus areas. No single definition can completely encompass the full scope of economics.

Notable Economists and Their Definitions

1. J.S. Mill

Mill described economics as the practical science concerned with the production and distribution of wealth.

2. A.C. Pigou

Pigou viewed economics as the science of material welfare. His approach centered on how total production could be enhanced to improve people's standard of living. He also defined economics in terms of wealth.

3. H.J. Davenport

Davenport defined economics as a subject that examines phenomena from the perspective of price. This definition emphasizes exchange and suggests that economics deals with anything possessing price value. According to this view, for a commodity or service to have economic significance, it must have an attached price.

4. Alfred Marshall

Marshall characterized economics as the study of humanity in the ordinary business of life. He maintained that economics encompasses the individual and social actions connected with acquiring the material requisites of well-being.

5. Adam Smith

The 18th-century British economist, often called "the father of Economics," defined economics as an inquiry into the nature and causes of nations' wealth. Smith's focus was primarily on wealth creation, and he established the foundation of economics as a distinct discipline.

The Generally Accepted Definition

While many definitions exist, one has gained widespread acceptance in the economic community:

6. Professor Lionel Robbins

Robbins defined economics as "a science which studies human behavior as a relationship between ends and scarce means which have alternative uses."

Robbins' definition is considered the most comprehensive as it is both analytical and scientific in nature. This definition has become the most popular and widely accepted among all economic definitions. Robbins categorized economics as a social science, emphasizing its study of human behavior in the context of resource allocation.

The Nature of Economics: Science and Social Science

Economics can be classified as both a science and a social science. It is considered a science because it employs systematic methods to study phenomena. Science, in a broad sense, is knowledge acquired through observation, testing, and the formulation of general principles. Similarly, economics uses the scientific method to explain observed economic events and predict future outcomes.

The Scientific Method in Economics

The scientific approach in economics involves a structured process:

- Observation of events and their outcomes

- Formulating a hypothesis

- Collecting relevant data

- Organizing and analyzing the data

- Formulating economic laws or theories

- Testing these laws

- Making predictions based on the established laws

However, economics is fundamentally a social science because it studies human behavior. As Professor Lionel Robbins pointed out, several basic facts define human economic life:

- Human wants are virtually unlimited.

- The resources available to satisfy these wants are limited or scarce.

- These scarce resources can be put to alternative uses.

The Main Branches of Economics

As a field of study, economics is broadly divided into two main branches: microeconomics and macroeconomics. While these concepts are closely related—both are concerned with the determination of prices, incomes, and the use of resources—they can be studied separately.

Microeconomics

Microeconomics focuses on the individual components of the economy. It examines the behavior of individual consumers, specific firms, and particular industries. This branch explains how the interactions between supply and demand help determine prices, wage rates, rental charges, and profit margins. For instance, microeconomics is concerned with how a single consumer reacts to price changes and their individual demand, rather than the total demand in the entire economy. Similarly, it analyzes the supply of one firm, not the aggregate national supply.

Macroeconomics

Macroeconomics, in contrast, examines the economy as a whole. It takes a comprehensive, national or even global viewpoint to analyze broad economic issues. Macroeconomics provides explanations for large-scale phenomena such as total employment, national production output, the general price level, economic growth rates, national consumption and investment, total exports and imports, economic booms and recessions, rates of inflation and deflation, and the overall level of national income.

Basic Concepts of Economics

Scale of Preference

A scale of preference is a list of unsatisfied wants organized by their priority or importance. This list serves as a crucial tool for decision-making, ensuring that the most pressing needs are addressed first when resources are limited.

Importance of Scale of Preference

- Helps individuals rank their needs in order of importance.

- Aids in the proper management of resources.

- Assists both individuals and governments in identifying the most critical needs.

- Promotes the optimal allocation of resources.

- Guides individuals, firms, and governments in the efficient utilization of resources.

- Helps economic agents maximize their satisfaction.

- Enables individuals to make rational decisions.

Opportunity Cost

Opportunity cost, often called the "real cost" or "alternative forgone," represents the value of the next-best option that is given up when a choice is made. It is the sacrifice incurred to select one alternative over another.

Example: If a student with N200 must choose between a book and a shirt that both cost N200, and they decide to buy the book, the opportunity cost is the shirt they did not purchase.

Relevance and Importance of Opportunity Cost

To Individuals:

- Guides individuals in making wise choices between competing wants.

- Enables individuals to make maximum use of scarce resources relative to their unlimited wants.

To Firms:

- Helps firms make rational decisions about their production processes.

- Aids industries in deciding on production techniques, such as choosing between capital-intensive or labor-intensive methods.

To Government:

- Assists the government in preparing the national budget by ensuring efficient allocation of scarce resources to key economic sectors.

- Helps in prioritizing decisions, such as identifying areas like healthcare and education that require immediate attention.

Resources

Resources are the inputs, or factors of production, used to satisfy human wants. These include productive assets like land, labor, capital, and entrepreneurship, which are essential for creating goods and services. Other key resources are time and money. A defining characteristic of resources is their scarcity—their supply is limited compared to the demand for them.

Types of Resources

- Economic Resources

- These are resources that have an opportunity cost because their supply is inadequate to meet the demand for them. Producers are willing to sacrifice other wants to obtain them.

- Non-economic Resources

- These are items whose supply is either inexhaustible or greater than the demand for them. They do not have an opportunity cost and are often considered "free" goods, such as air and water.

- Natural Resources

- These refer to minerals and materials found in the natural environment, such as coal and crude oil.

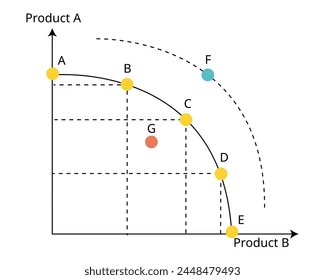

Production Possibily curve

PPC is a curve or graph that shows the combination of two commodities that can be produced, given the available resources and state of technology.The slope of the PPC is sometimes called the Marginal Rate of Transformation.

The PPC is used to represent production possibility table i.e the graphical representation of the data in a PPC schedule (table) actually gives the production possible curve. It shows the various possible or attainable and non attainable combinations or maximum output a producer can produce with a given unit of economic resources, hence it is also called production feasibility curve (PFC). The production possibility curve (PPC) is a practical application of the principle of opportunity cost.

Credit: Piscine26 on

Shuttershock

Credit: Piscine26 on

Shuttershock

Point G located inside the PPC implies that the country is not able to make efficient use of all the existing resources. Points located inside the curve are called ‘Inefficient production combinations’.

Point F located outside the curve is viewed as unattainable production combination because the country does not have enough resources to produce a larger combination of goods than the combinations indicated on the curve

Outward Shift of the PPC

An outward shift of the Production Possibility Curve (PPC) indicates economic growth and development. It means that the economy can now produce more goods and services than before due to improvements in productive capacity.

The outward shift may result from the following factors:

- More efficient utilization of resources such as land, raw materials, and capital goods.

- An increase in the stock of capital goods.

- Improvement in production techniques and technology.

- Higher productivity (increase in output per worker per hour).

- Growth in the size of the labour force, especially skilled labour.

- Discovery or extraction of additional natural resources, such as crude oil.

- Establishment of more industries or a major economic boom.

Inward Shift of the PPC

An inward shift of the PPC reflects a decline in an economy’s productive capacity. This means the economy can produce fewer goods and services than before.

The inward shift may be caused by the following factors:

- Less efficient use of resources such as land, raw materials, and capital goods.

- A reduction in the labour force, especially skilled workers.

- A severe economic recession or slump.

- A decline in productivity (reduced output per worker per hour).

- An increase in unemployment and underemployment.

- Exhaustion of natural resources, such as crude oil.